If you’ve just received your first salary, paid off your education loan, or simply realised that your bank balance never seems to grow no matter how much you earn — you’re exactly where most Indians are. The truth is, schools don’t teach personal finance, and most of us learn it the hard way: through missed EMIs, impulse buys, and tax surprises in March.

This complete guide is built to fix that. By the end of it, you’ll know how to manage personal finances, build a budget that actually works in Indian households, save smartly, start investing with even ₹500 a month, and avoid the mistakes that quietly drain wealth in your 20s and 30s.

At Profito, we work with hundreds of clients across Delhi NCR who started exactly where you are now — and reached financial independence faster than they thought possible. Let’s walk you through the same framework.

What You’ll Take Away From This Guide

▸ A clear, India-specific framework to manage your money from your very first salary

▸ How to budget, save, and invest using the 50-30-20 rule adapted for Indian metros

▸ Exact instruments to use — PPF, SIPs, ELSS, NPS — and which to avoid

▸ How to save up to ₹46,800 in tax annually under Section 80C

▸ The 7 lifelong guidelines and the common mistakes Indian beginners make

What Personal Finance Actually Means (and Why It’s Different in India)

Personal finance is simply the management of your money — your income, expenses, savings, investments, insurance, and future goals. But in India, the rules of the game look slightly different from what you’ll read on US or European blogs.

Here’s why:

- Joint family responsibilities often mean supporting parents or siblings, not just yourself.

- Cash culture still influences how we track expenses, especially in tier-2 and tier-3 cities.

- Real estate and gold are deeply rooted as wealth instruments — sometimes at the cost of better-performing investments.

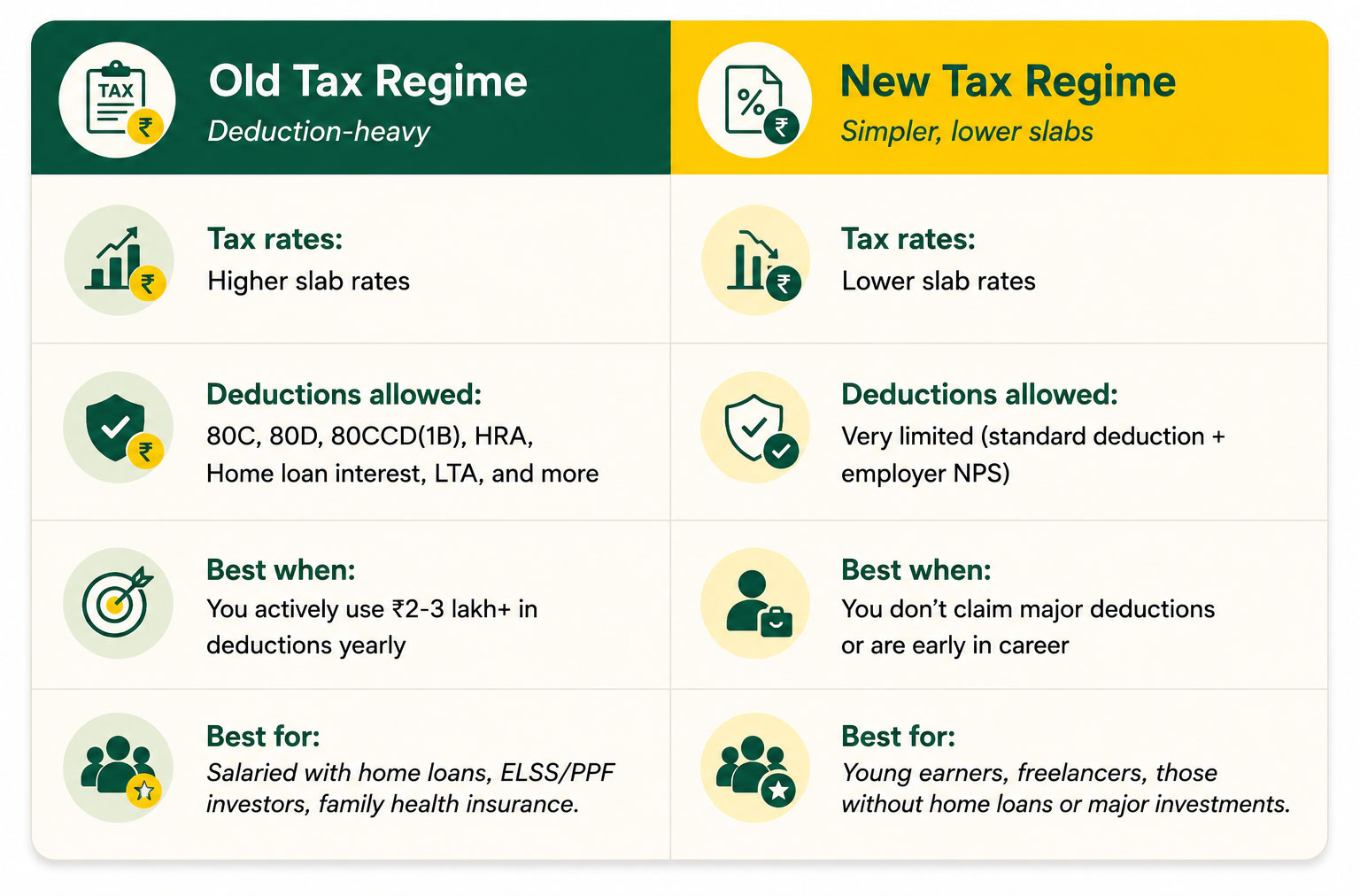

- Tax structures like Section 80C, 80D, and the new vs. old tax regime under Union Budget 2026 require specific planning.

- EMIs are everywhere — phones, cars, education, weddings — and most beginners underestimate how much they erode long-term wealth.

So while global principles like “spend less than you earn” hold true, the Indian execution needs its own playbook. This guide gives you exactly that.

Step 1: Audit Where You Stand Today

Before you plan where to go, find out where you are. Most beginners skip this and jump straight to investing — that’s a mistake.

Sit down for 30 minutes and write down four numbers:

- Your monthly take-home income (after tax and PF deductions)

- Your total monthly expenses (rent, EMIs, groceries, subscriptions, food delivery, transport — everything)

- Your total assets (savings account balance, FDs, mutual funds, EPF, gold, property)

- Your total liabilities (credit card outstanding, personal loans, education loan, home loan, money owed to family)

Subtract liabilities from assets — that’s your net worth. It can be negative when you’re starting out, and that’s perfectly fine. The point is to know the number, because every decision from here on either increases or decreases it.

Step 2: Build a Budget That Survives Real Life

A budget isn’t a punishment — it’s permission to spend on what actually matters to you. The most popular framework, adapted for Indian incomes, is the 50-30-20 rule:

- 50% on Needs — rent, groceries, utilities, transport, EMIs, insurance premiums

- 30% on Wants — dining out, OTT subscriptions, travel, shopping, hobbies

- 20% on Savings & Investments — SIPs, emergency fund, retirement, goal-based savings

If you earn ₹60,000 a month in-hand, that’s ₹30,000 for needs, ₹18,000 for wants, and ₹12,000 going straight into your future.

But here’s the honest part — in metros like Delhi, Gurgaon, Noida, or Bengaluru, rent alone can eat up 30-35% of your income. In that case, adjust to a 60-20-20 or even 70-15-15 split. The exact percentages matter less than the discipline of paying yourself first — automate that 20% before you spend a rupee on anything else.

How to Make Your Budget Stick

- Automate transfers on salary day — SIP on the 2nd, RD on the 3rd, emergency fund on the 4th.

- Use separate accounts — one for fixed expenses, one for daily spends, one for savings.

- Review weekly, not monthly — by the time the month ends, the damage is done.

- Allow guilt-free spending in the “wants” bucket. Strict budgets fail; flexible ones survive.

Step 3: How Much Emergency Fund Should You Have in India?

Before you invest a single rupee in stocks or mutual funds, build an emergency fund equal to 6 months of essential expenses. If you’re self-employed or in a volatile industry, make it 9-12 months.

For someone with monthly expenses of ₹40,000, that’s ₹2.4 lakh sitting in a place where you can access it within 24-48 hours but won’t be tempted to touch.

Where to park your emergency fund in India:

- High-interest savings accounts (some private and small finance banks offer 6-7% on balances above ₹1 lakh)

- Liquid mutual funds (returns of 6-7%, redeemable in 1 working day)

- Sweep-in fixed deposits linked to your savings account

- Short-term FDs with auto-renewal

Avoid keeping it in regular savings (3-3.5% return loses to inflation) or locking it in long-term FDs where premature withdrawal eats into returns.

Also Read : Top Stock Market Strategies

Profito tip: This is the single step that separates people who recover from a job loss or medical emergency in weeks vs. those who fall into debt for years. Don’t skip it.

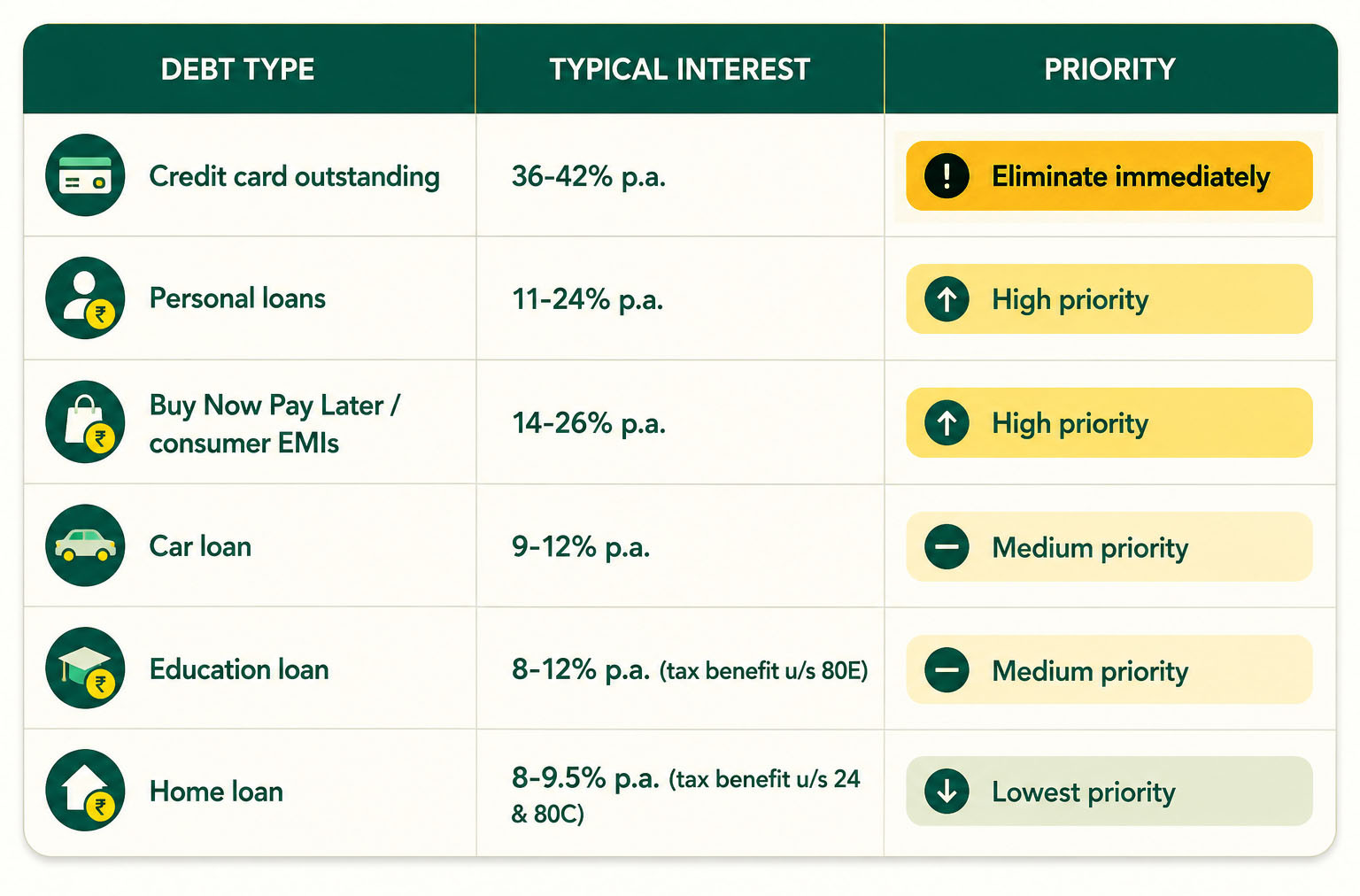

Step 4: Crush High-Interest Debt Before You Invest

Here’s a math truth most beginners miss: if your credit card charges 36-42% interest annually, no investment will reliably beat that. Paying off that debt is the highest-return investment available to you.

Prioritise debt in this order:

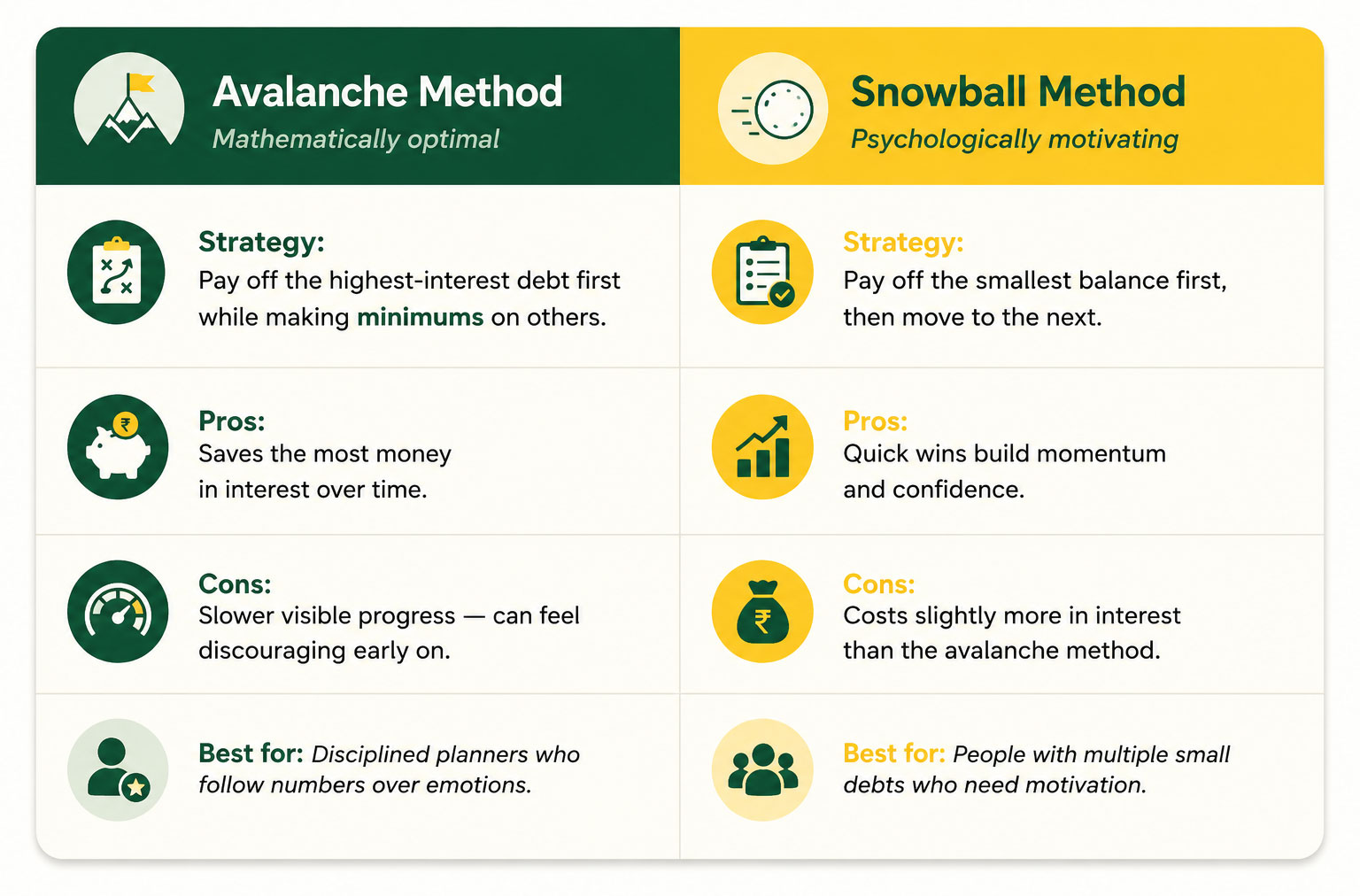

Use the avalanche method (pay off highest-interest debt first while making minimums on others) for maximum savings. Use the snowball method (smallest balance first) if you need psychological wins to stay motivated.

Step 5: Understand the Indian Investment Landscape

Once your emergency fund is in place and high-interest debt is under control, you’re ready to invest. Here are the main options available to Indian retail investors, from safest to most aggressive:

Fixed Income / Low Risk

- Public Provident Fund (PPF) — 15-year lock-in, ~7.1% tax-free, EEE category

- Fixed Deposits (FDs) — 6.5-7.5%, taxable

- Recurring Deposits (RDs) — disciplined monthly savings

- Government Bonds & RBI Floating Rate Bonds — safe, long-tenure

- Sukanya Samriddhi Yojana — for parents of girl children, ~8.2% tax-free

Hybrid / Moderate Risk

- National Pension System (NPS) — retirement-focused, extra ₹50,000 deduction u/s 80CCD(1B)

- Hybrid mutual funds — mix of equity and debt

- Corporate FDs — higher returns than bank FDs but check credit ratings

Equity / Higher Risk, Higher Return

- Equity mutual funds via SIP — the easiest entry point for beginners, Read deep-dive on how SIPs create long-term wealth

- Index funds & ETFs — low cost, track Nifty 50 or Sensex

- ELSS funds — equity + tax savings under 80C, 3-year lock-in

- Direct stocks — only after you understand fundamentals

Alternative

- Gold ETFs / Sovereign Gold Bonds — better than physical gold for investment purposes

- REITs (Real Estate Investment Trusts) — exposure to commercial real estate without buying property

You don’t need to invest in all of these. Most beginners do well with just three or four instruments: PPF + EPF for safety, equity mutual funds for growth, and a Sovereign Gold Bond or two for diversification.

Step 6: Start Investing — Even If You Have Just ₹500

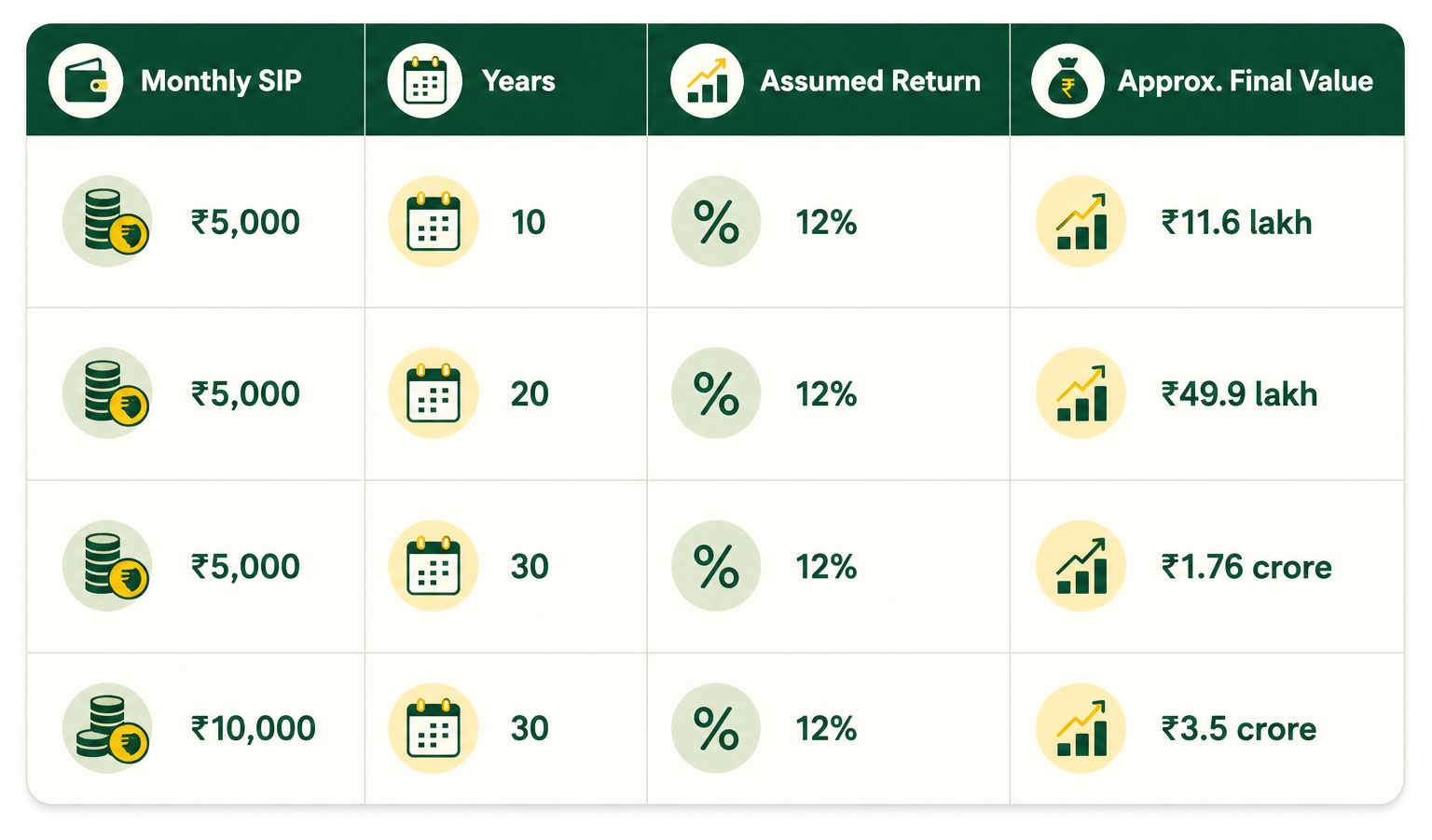

This is where most beginners freeze. They wait until they “have enough” to start. But thanks to Systematic Investment Plans (SIPs), you can begin with as little as ₹500 a month.

Here’s the magic of starting early — the power of compounding:

The same ₹5,000 SIP becomes 15x more valuable just by starting 20 years earlier.

Time in the market beats timing the market.

See our detailed breakdown on how investment time horizon impacts your returns

How to Start Your First SIP (Step-by-Step)

- Complete your KYC through any AMC website or apps like Groww, Zerodha Coin, Kuvera, or ET Money.

- Pick a fund category — for beginners, an index fund tracking Nifty 50 or a Nifty Next 50 fund is ideal.

- Set a monthly amount you can sustain — start small if needed.

- Choose direct plans (lower expense ratio) over regular plans.

- Automate it through a bank mandate so it happens every month without you thinking about it.

- Review annually, not weekly. Equity volatility is normal; reacting to it is what destroys returns.

Step 7: Best Tax-Saving Investments in India for Beginners

If you’re under the old tax regime, you can save up to ₹46,800 in tax annually through Section 80C alone (for those in the 30% bracket). The trick is choosing instruments that save tax and build wealth — not just tax-saving products you’ll regret.

Section 80C — ₹1.5 lakh limit (best options for beginners):

- ELSS mutual funds — shortest lock-in (3 years), highest long-term returns

- PPF — safe, tax-free, long-term

- EPF — already happening if you’re salaried; check your contribution

- Tax-saving FDs — 5-year lock-in, lower returns, fully taxable interest

- Life insurance premium — only if you actually need the cover; avoid ULIPs and endowment plans purely for tax saving

Beyond 80C:

- Section 80CCD(1B) — extra ₹50,000 deduction for NPS contributions

- Section 80D — health insurance premiums (₹25,000 for self/family + ₹50,000 for senior citizen parents)

- Section 24(b) — up to ₹2 lakh on home loan interest

- Section 80E — education loan interest (no upper limit, for 8 years)

Under the new tax regime, most of these deductions don’t apply — but tax slabs are lower. Compare both regimes annually using the Income Tax Department’s calculator before filing.

Step 8: How to Plan Retirement in Your 20s and 30s

Retirement feels distant when you’re 25, but it’s the single goal most Indians underestimate. With increasing life expectancy and no formal social security, you’re likely to need 20-25x your annual expenses by retirement.

A simple rough target: if you need ₹50,000/month to live in today’s value, factoring in 6% inflation over 30 years, you’ll need around ₹6-7 crore by age 60.

Sounds intimidating? Here’s the breakdown:

- EPF (12% of basic from you + 12% from employer) builds a strong base passively

- NPS (additional ₹50,000 + employer contribution) adds to it

- Equity SIPs (₹15,000-25,000/month started in your late 20s) typically fill the rest

Start with whatever you can. Even a ₹3,000 SIP at age 25 is worth more than a ₹15,000 SIP started at 40.

The 7 Personal Finance Guidelines Every Beginner Should Follow

If you remember nothing else from this guide, remember these:

- Spend less than you earn — the foundation of everything.

- Pay yourself first — automate savings on salary day, not at month-end.

- Get adequate insurance early — term life + health insurance are non-negotiable. Skip ULIPs and money-back policies.

- Avoid lifestyle inflation — when your salary jumps 30%, don’t let your expenses jump 30%.

- Diversify but don’t over-diversify — 4-6 quality instruments are enough.

- Never invest in something you don’t understand — including crypto, F&O, or any “guaranteed return” scheme.

- Keep learning — read one personal finance book a year. Start with Let’s Talk Money by Monika Halan or The Psychology of Money by Morgan Housel.

Common Mistakes Indian Beginners Make

After advising hundreds of clients across Delhi, Gurgaon, Noida, and Ghaziabad, these are the patterns we see again and again:

- Buying expensive insurance disguised as investment (ULIPs, traditional endowment plans, money-back policies). Always separate insurance from investment.

- Real estate as the only investment — illiquid, high entry barrier, often gives lower returns than equity over long periods.

- Trying to time the stock market — beginners enter at peaks and exit at lows. Stay invested through SIPs.

- Ignoring health insurance because the company provides it — corporate policies vanish the day your job does.

- Saving without investing — money in a savings account loses to inflation every single year.

- Following stock tips from WhatsApp groups, YouTube influencers, or relatives — most are unqualified and many are paid promotions.

- Treating EMIs as “small monthly amounts” — six concurrent EMIs add up to financial bondage.

- Not having a will — even for unmarried 30-year-olds. It costs almost nothing and saves families from years of disputes.

When Should You Speak to a Financial Advisor?

You can absolutely manage the basics yourself with the discipline outlined above. But there are moments when professional advice pays for itself many times over:

- You’ve crossed ₹15-20 lakh in investible savings and don’t know how to allocate

- You’re getting married, buying a house, or starting a family

- You’ve received a windfall — bonus, inheritance, ESOP exit

- You’re a freelancer or business owner with irregular income

- You’re approaching retirement and need a withdrawal strategy

- You feel constantly anxious about money despite earning well

A good advisor — especially a SEBI-registered fee-only planner — won’t just sell you products. They’ll build a roadmap aligned to your goals, optimise your tax outflow, and help you avoid emotional decisions in volatile markets.

At Profito, we offer personalised financial planning and investment advisory services across Delhi NCR — Delhi, Gurgaon, Noida, Faridabad, and Ghaziabad. Whether you’re just starting out or restructuring an existing portfolio, our advisors design plans that fit your life, not the other way around.

| Quick Recap — The 7 Pillars to Remember

▸ Audit your net worth before doing anything else — you can’t improve what you don’t measure ▸ Budget with the 50-30-20 rule, adjusted for your city’s reality ▸ Build a 6-month emergency fund BEFORE you invest a rupee ▸ Crush high-interest debt — it’s the highest-return ‘investment’ you can make ▸ Start SIPs with whatever you can — even ₹500/month — and let compounding do the rest ▸ Use 80C, 80CCD(1B), 80D, and 24(b) to optimise tax — but only with instruments you’d buy anyway ▸ Separate insurance from investment. Always. Term + Mutual Fund beats ULIP every time. |

Frequently Asked Questions (FAQs)

Q1. How much should a beginner invest every month in India?

Start with at least 20% of your take-home income. If that’s not possible, even 10% is a solid beginning — the habit matters more than the amount in year one.

Q2. Is SIP better than FD for beginners?

For long-term goals (5+ years), SIPs in equity mutual funds historically deliver 11-13% annualised returns vs. 6-7% from FDs. For short-term goals (under 3 years) or emergency funds, FDs and liquid funds are better.

Q3. What’s the safest investment for a complete beginner in India?

PPF, EPF, Sukanya Samriddhi (if eligible), and Government Bonds are the safest. For slightly higher returns with low risk, consider liquid funds or sweep-in FDs.

Q4. Should I clear my home loan early or invest the surplus?

If your home loan rate is 8.5% and you can earn 11-12% post-tax in equity over the long term, investing wins mathematically. But if debt makes you anxious, partial pre-payment offers peace of mind that’s hard to put a number on.

Q5. What is the 50-30-20 rule and does it work in India?

It’s a budgeting framework — 50% needs, 30% wants, 20% savings & investments. It works as a starting point, but in metros with high rents, you may need a 60-20-20 split until your income grows.

Q6. Do I need a financial advisor if I’m earning ₹6-8 lakh per annum?

Not necessarily — basic discipline and the steps in this guide will take you far. Consider an advisor when your investments cross ₹10-15 lakh, your tax planning gets complex, or major life events arise.

Q7. What’s the difference between term insurance and life insurance?

Term insurance is pure protection — pay a small premium, get a large cover, no payout if you survive the term. Life insurance often refers to ULIPs or endowment plans that mix insurance and investment poorly. For beginners: buy term insurance, invest the difference in mutual funds.

Final Word

Managing your money well isn’t about complicated formulas or chasing the next hot stock. It’s about a few simple habits — spending less than you earn, automating savings, investing consistently in good instruments, protecting yourself with insurance, and avoiding lifestyle creep.

Do these for ten years and you’ll quietly outpace 95% of people who earn far more than you but never built a system.

If you’d like a personalised plan built around your income, goals, and risk appetite, book a free consultation with Profito’s advisory team. We help individuals and families across Delhi NCR transform anxiety about money into a clear, confident plan.

Your future self will thank you for starting today.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks; please read all scheme-related documents carefully. For personalised advice, consult a SEBI-registered investment advisor.