Let me guess something about you.

Your salary crossed ₹2 lakh a month somewhere in the last few years. Maybe you’re at ₹3 now. Maybe ₹4. And the day that number first hit your account, some part of you exhaled and thought — I’ve made it.

Now open your bank app. Go on, I’ll wait. What’s the balance actually saying?

Yeah. That’s what I thought.

I’m not writing this to make you feel good. I’m writing it because in all my years sitting across the table from people who earn well, I’ve learned one thing that nobody says out loud at the office party: a shocking number of high earners are one missed salary away from disaster. Not because they earn too little. Because nobody ever told them that hitting a number is not the finish line.

It’s the starting gun for a completely new game. And this one is quietly designed to bankrupt you.

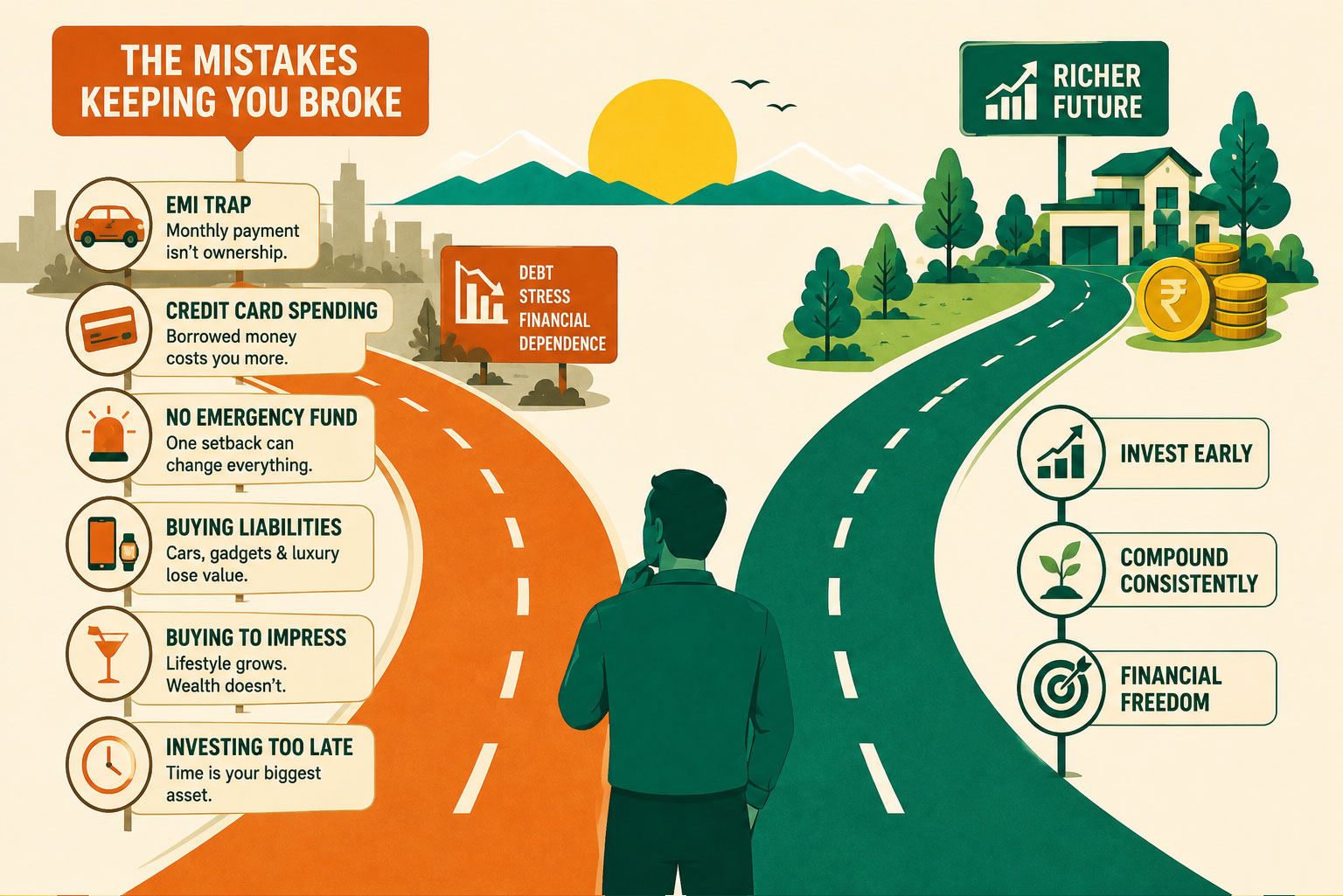

The trap has a name, and you’re already in it

Watch how familiar this feels.

The promotion comes. Income jumps. And within about three months, so does everything else. The 1BHK becomes a 3BHK. The old car becomes an SUV — on EMI, obviously, because “the monthly is manageable.” The phone gets upgraded every year now. Weekends are Goa. Saturday nights are ₹8,000 bar tabs. Dinner for two casually crosses ₹3,000, because hey, you’ve earned it.

Your income went up 40%. Your lifestyle went up 60%.

And you genuinely, honestly cannot understand why ₹4 lakh a month feels tighter than ₹1 lakh did five years ago.

That’s not bad luck. That’s a law. Your expenses will always rise to swallow whatever you earn — unless you consciously stop them. And almost nobody stops them. That is the entire trap, and you fell into it the day you started measuring success by how much came in instead of how much stayed.

The exact mistakes you’re making right now

Let me be blunt, because soft advice has never made anyone rich. Here’s what I actually see, on repeat, in people just like you:

You think “I can afford it” means “I can afford the EMI.” You cannot afford a ₹20 lakh car. You can afford ₹35,000 a month for seven years — which is a very different, and much more expensive, sentence. The EMI is the leash. You just volunteered for it.

You treat your credit card limit like it’s your money. It is not your money. It is the bank’s money, rented to you at roughly 40% a year — the single most expensive loan a human being can take on — and you’re taking it to buy sushi and sneakers.

You have no emergency fund. Be honest with yourself. If your income stopped tomorrow, how many months could you actually survive? For most ₹2-lakh earners, the real answer is less than two. You are one layoff, one health scare, one bad quarter away from the whole thing coming down.

You buy liabilities and call them assets. A car is not an asset. A phone is not an asset. That watch is not an asset. An asset puts money into your pocket. Almost everything you’re proud of owning is quietly taking money out of it, every single month.

You’re spending to be seen. The parties, the brands, the round of drinks you insist on buying, the story you post from the club — a huge chunk of your money isn’t buying you happiness. It’s buying you other people’s approval. And here’s the punchline: those people are broke too. Stressed too. Posting the exact same lie you are.

And the big one, the one that costs you the most: you invest almost nothing, and you started late.

Read: A Complete Guide to Managing Better Finance and Investment For Beginners.

Now here’s the part that’s going to sting

Let me show you the math, because feelings lie and math doesn’t.

Person A earns ₹2 lakh a month. Spends ₹1.9 lakh. Invests ₹10,000. Feels rich.

Person B earns ₹80,000 a month. Spends ₹50,000. Invests ₹30,000. Feels “behind.”

Fast forward 15 years, at roughly 12% a year — the long-run ballpark for equity, not a promise, markets move:

- Person A’s ₹10,000/month → about ₹50 lakh

- Person B’s ₹30,000/month → about ₹1.5 crore

The guy earning less than half of you ends up three times richer.

Read that again. Slowly.

Your income was never the thing that made you wealthy. The gap between what you earn and what you spend — that is the only thing that has ever mattered. And right now, if you’re honest, your gap is basically zero.

That ₹8,000 you dropped on cocktails last Saturday? As a one-off, it’s nothing. As a weekly habit — around ₹32,000 a month — invested instead, it’s the difference between retiring free and working until the day you drop. You’re not buying drinks. You’re setting fire to your future one weekend at a time, and calling it “living my life.”

Read our related blog on Investment Horizon Explained: How Time Impacts Your Returns.

So what do you actually do about it

Now breathe, because I’m not here to make you feel like garbage. I’m here to hand you the exit. And the exit is smaller and harder than you think, because it isn’t about money at all. It’s about your head.

Pause. Before the next upgrade, the next EMI, the next “I deserve this” — just stop and calculate the full cost, not the monthly one. Most bad money decisions die the moment you do the real math.

Define your “enough.” Almost nobody has a number. And without one, no salary on this earth will ever feel like enough — you’ll chase the horizon until you’re 60 and exhausted. Decide what a genuinely good life costs you, and aim at that instead of at “more.”

Pay yourself first. Not with whatever’s left at the end of the month — there’s never anything left, and you know it. Automate your investment on the 1st, before your lifestyle gets its hands on the money, and force yourself to live on the rest. Discipline you have to remember every day will fail. Discipline you set up once will hold.

Get insured properly — and stop mixing insurance with investment. A term plan protects your family. Your investments grow your money. The endowment and ULIP products dressed up as “savings schemes” quietly rob you of both at the same time. Keep them separate.

Then let compounding do the boring, beautiful work while you sleep, while you’re at meetings, while you’re on holiday. That’s the whole secret. It was never about being brilliant. It was about being consistent and patient long enough for the math to become unfair in your favour.

The point I actually want you to walk away with

Here’s what I believe, underneath all the bluntness.

Money is not the goal. Freedom is. Being able to say no. Being able to take the risk, take the year off, take care of your parents without checking the balance first, walk away from the job that’s slowly killing you.

Money is just the tool that buys you that freedom. And right now, you are handing that tool away — every weekend, every EMI, every upgrade — to look impressive to people who genuinely do not care about you.

That’s the real game. Not more zeros on your payslip. A life you’re not quietly panicking behind.

One honest conversation

I’ll be straight with you, because at Profito that’s the only way we know how to work. We don’t sell dreams and we don’t do “guaranteed 20% returns” nonsense. What we do is unglamorous: we help you fix the gap, build the system, and — most importantly — fix the mindset underneath it. Because your money problem was never really a math problem. It was a behaviour problem. And behaviour is exactly what we mentor people through.

We’re AMFI-certified. Our mutual fund consultations cost you nothing. And we’ll tell you the uncomfortable truth long before we tell you what you want to hear.

So if you’re tired of earning well and still feeling broke — if some line in this hit a little too close — let’s talk. One honest conversation. No pitch you didn’t ask for.

Because earning ₹2 lakh a month and dying broke is a choice.

You just have to stop making it.

Read more: How SIP in Mutual Funds Helps Create Wealth.

Ready when you are — book a free consultation or call us at +91 97495 77794.

Disclaimer: Mutual funds and investments in the equity market are subject to market risks. Please read all related documents carefully. Returns mentioned above are illustrative, assume long-term equity averages, and are not guaranteed.

Frequently Asked Questions

1. Why do many people earning ₹2 lakh or more per month still struggle financially?

A high income alone doesn’t create wealth. Many high earners increase their lifestyle expenses as their salary grows, leaving little room for saving or investing. Wealth is built by the gap between what you earn and what you keep.

2. What is lifestyle inflation, and why is it dangerous?

Lifestyle inflation is the tendency to spend more as your income increases. Bigger homes, expensive cars, luxury vacations, and frequent upgrades can consume salary increases, making it difficult to build long-term wealth despite earning more.

3. How much of my salary should I invest every month?

A common guideline is to invest at least 20–30% of your income, depending on your financial goals and obligations. The key is to automate investments before discretionary spending so that investing becomes a habit rather than an afterthought.

4. Why is paying yourself first considered a smart financial habit?

Paying yourself first means investing before spending on lifestyle expenses. By automating investments on your salary day, you prioritize wealth creation instead of relying on whatever money is left at the end of the month.

5. How much emergency fund should I have?

Financial planners generally recommend maintaining an emergency fund that can cover 6 to 12 months of essential living expenses. This provides a financial cushion during job loss, medical emergencies, or unexpected expenses.

6. Why should I avoid making decisions based only on EMI affordability?

An affordable monthly EMI doesn’t necessarily mean you can truly afford the purchase. Always evaluate the total ownership cost, including interest, maintenance, insurance, and the long-term impact on your savings and investments.

7. Why is investing early more important than earning a higher salary?

Starting early gives your investments more time to benefit from compounding. Even smaller, consistent investments made over many years can potentially grow into a larger corpus than bigger investments started much later.

8. Should insurance and investments be kept separate?

Yes. Insurance is designed to protect your family financially, while investments are meant to build wealth. Many financial experts recommend buying adequate term insurance and investing separately through suitable investment products.

9. What is the biggest mistake high-income earners make?

One of the biggest mistakes is assuming that a higher salary automatically leads to wealth. In reality, uncontrolled spending, excessive debt, delayed investing, and lack of financial planning often prevent high earners from building meaningful wealth.

10. How can Profito help me improve my financial habits?

Profito offers AMFI-certified mutual fund consultation and personalized financial guidance to help you build better money habits, create a disciplined investment strategy, and work toward long-term financial goals. Mutual fund investments are subject to market risks, and all investment decisions should be based on your individual financial situation and objectives.