Most investors focus on choosing the right product or chasing better returns, but the real game-changer in investing is time. How long you stay invested can shape not only your returns but also your ability to handle risk and stay consistent. This simple idea is called your investment horizon, and it quietly determines how your money behaves over time.

Understanding it helps you see why patience often outperforms timing and how the right duration can turn regular investing into meaningful wealth creation. In this guide, we’ll explore how time truly impacts your returns and why it’s the foundation of every successful investment plan.

What is an Investment Time Horizon?

An investment time horizon is the amount of time you plan to leave your money invested before you need it. It helps you decide where to invest and how much risk you can safely take.

For example, if Amit is saving for a holiday next year, he can say that the time horizon is short. He needs this money soon, so he should invest in safer options like fixed deposits or liquid mutual funds that protect his capital. On the other hand, Naira is planning to invest for retirement 20 years from now. This is a long time horizon. Both of their investment horizons will be different and so will be the returns.

Your investment horizon affects your returns because of the power of compounding. The time you give your money directly affects the level of risk you can take and the returns you can expect. The longer your investment stays untouched, the greater its potential to build wealth.

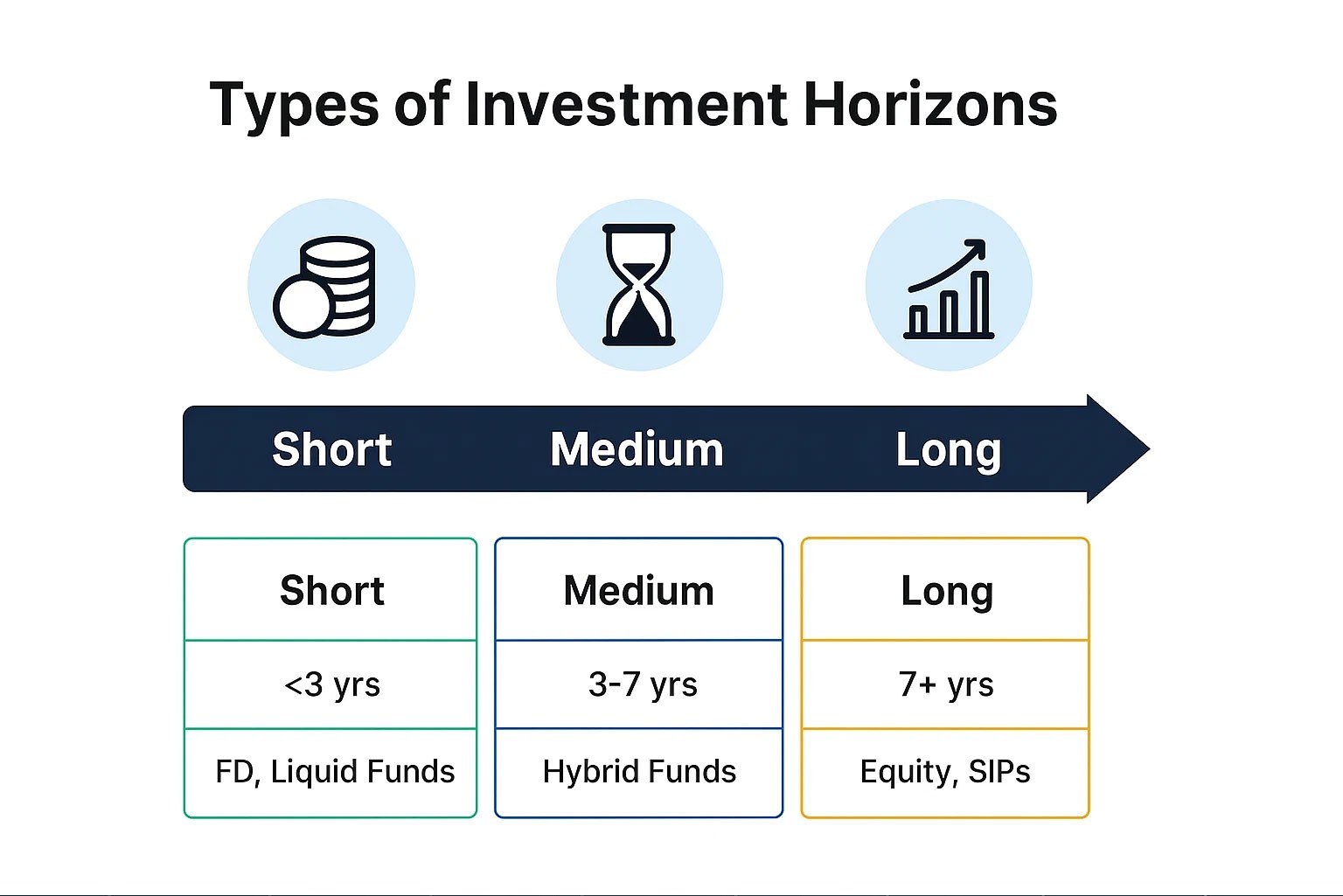

1. Short-Term Investment Horizon

If your investment horizon is short-term, you intend to utilize your money in the next 1 to 3 years. Because of the length of time, a minor change in the market can have a significant impact on your investment. Therefore, when thinking about short-term investments, you should have a priority of capital preservation, not returns. You want to ensure your money is guaranteed safe and available to you when you need it instead of being tied up in a risky investment.

2. Medium-Term Investment Horizon

A medium-term investment horizon offers a balance between growth and safety. Since the goal is a few years away, you can take moderate risk but not enough to rely fully on equities. A mix of stable and growth-oriented investments works best here. Typical goals include buying a car, making a home down payment, or funding a child’s education, where steady progress matters more than quick gains.

3. Long-Term Investment Horizon

A long-term investment horizon usually spans seven years or more and is ideal for building lasting wealth. Over time, your investments benefit from compounding, where returns start generating additional returns. Short-term market swings matter less as the overall trend favors growth. Goals such as retirement, children’s education, or wealth creation fit this horizon, where consistent investing can turn small contributions into significant future value.

What is the Ideal Investment Horizon?

The “ideal investment horizon” refers to the time period that best suits your investment objectives, risk tolerance, and need for returns. There is not one “ideal” number of years that everyone should match to.

The best investment horizon is one allowing your money sufficient time to grow without necessitating excessive risk-taking. It needs to be plenty long for you to take advantage of compounding returns but realistic enough in the context of your own life plan.

The longer the investment horizon, the more opportunity you have to buy high-return, high-risk assets, such as equities, which can exhibit volatility in the near term but appreciate quite dramatically over the long term.

How to Decide Your Investment Time Horizon?

The first step in determining your investment time horizon is understanding your financial objective and when you anticipate needing those funds. The more specific your objective is, the easier it will be to determine how long to stay invested.

For example, Shweta plans to buy a house in five years, giving her a medium-term investment horizon. Abhinav, on the other hand, is investing for his child’s education fifteen years from now, which makes his investment horizon long-term. The key is to tie every investment to a purpose and a timeframe.

When you have established your goal, think about how much risk you wish to take on. If your time horizon is longer, you will be able to take on more risk since you have a longer time frame to recover from market fluctuations. While a shorter horizon will let you focus on safe investments to protect your capital.

Lastly, consider your income stability and the stage of your personal life. It is much easier for a younger professional to select a long-term time horizon, whereas someone closer to retirement will focus on short-term or medium-term goals. By balancing your financial objectives with risk tolerance and life events, you can select a time horizon that achieves your goals without causing undue financial pressure.

How Investment Horizons Impacts Your Returns

- Compounding:

The time you stay invested has a powerful impact on how your money grows. Investing is not just about picking the right product, but about giving it enough time to perform. When your money remains invested, it benefits from compounding, a process where your returns start generating their own returns. Over the years, this steady growth can transform small, regular investments into significant long-term wealth.

- Behaviour and Volatility:

Your investment horizon also influences how you handle market fluctuations. When your goals are clear, it becomes easier to stay calm and avoid emotional decisions during market ups and downs. Investors who plan their timelines and stick to them often experience more stable, consistent growth. In investing, patience and discipline matter just as much as strategy, turning time itself into a key driver of lasting returns.

What are the Factors that Affect Investment horizons

1. Financial Goals

The amount of time you should invest for is based on your goal. Short-term goals such as buying a new gadget or going on vacation have a shorter time horizon. Long-term goals such as saving for retirement or children’s education will require a longer time horizon so your wealth can compound over time.

2. Age and Life Stage

Young investors have a long-term horizon and can take more risk because they have time. A person close to retirement needs safer, shorter-term investments because they need the money soon.

3. Risk Tolerance

If you’re okay with market fluctuations, you can opt for a longer horizon and invest in higher-risk assets to garner larger returns. If you like stability, you will select a shorter investment horizon with low-risk portfolios.

4. Income Stability

A steady income allows you to stay invested longer without needing withdrawals. If your income is uncertain, a shorter investment horizon helps maintain liquidity and safeguards against unexpected financial needs.

5. Liquidity Needs

If you’re anticipating needing funds for an emergency or a planned expense soon, your investment horizon will be shorter. If you don’t need funds immediately, you can invest for the longer-term.

6. Inflation and Economic Conditions

When planning for long-term goals, it is important to consider inflation, as it reduces the value of money over time. To overcome this, you need investments that offer higher returns and preserve real wealth.

What are the Risks while using Investment Time Horizons?

1. Market Volatility

Investors may experience sudden market declines, and if investing for the wrong length of time for their financial goal, the investor is likely to sell at a loss. If money is invested in risk assets short term, there may not be enough time for assets to recover if the market unexpectedly declines. This is the danger of capital erosion, instead of realizing a return on capital.

2. Misjudging the Time Needed

Some investors presume that the money will not be needed for many years. However, life events like health emergencies, job relocation and family requirements can shorten the timeline. When that occurs, long-term investments may not be liquid or time appropriate for withdrawal and can result in stress or penalties.

3. Inflation Risk

When investing with a very short timeframe for a long-term goal, you may resort to selecting extremely low-return investments in situations where the return does not beat inflation. While this may help you feel more secure about your investment, the investment’s real value will decline over time (the real value is the purchase power that investment can provide), thereby impacting your ability to accomplish your long-term financial goals.

4. Liquidity Risk

There are some long-term investments, like real estate or pensions, that come with constraints or prolonged lock periods. If you need access to cash right away, you will not be able to access your money without incurring penalties or selling your investment at an unwanted time, which would weaken your financial state.

5. Overexposure to Risky Assets

Diversification helps reduce this risk by spreading investments across different assets. It ensures that poor performance in one area does not significantly impact overall returns, keeping your portfolio balanced and stable.

6. Goal Mismatch

Investing in the wrong asset for your goal’s timeline can cause financial stress. For instance, short-term goals in equities may force untimely withdrawals during volatility, disrupting your progress toward planned objectives.

Time-Based Asset Allocation Strategy for Indian Investors

Asset allocation means spreading your investments across equity, debt, gold, and real estate in a way that suits your goals and comfort with risk. It ensures that every part of your portfolio has a clear purpose and works together toward steady growth. In a changing market like India’s, linking your investment mix to your financial goals helps you stay consistent and prepared.

A good allocation strategy is not fixed forever. As your goals and market conditions evolve, your portfolio should adapt too. Regularly reviewing and adjusting your investments keeps them aligned with your priorities and builds wealth in a disciplined and confident way.

Common Mistakes to Avoid

Investing Without a Clear Goal

Investing without defining a specific goal or timeline can lead to confusion and poor results. When you don’t know when you will need the money, you may choose the wrong product. A clear goal helps you pick the right investment horizon and ensures your money grows in the right direction.

Using Risky Investments for Short-Term Goals

Short-term goals require safety and liquidity, not high returns. Investing in stocks or equity mutual funds for goals that are one to three years away can be risky. A sudden market drop could force you to sell at a loss, leaving you short of money when you need it most.

Being Too Conservative for Long-Term Goals

When your goal is many years away, being overly safe can harm your growth. Keeping long-term investments only in fixed deposits or savings accounts may protect capital but fail to build wealth. Such conservative choices often cannot beat inflation, reducing your ability to meet long-term financial goals comfortably.

Ignoring Inflation

Inflation reduces the purchasing power of your money over time. If you invest in low-return products without considering inflation, your savings may grow in numbers but lose real value. For long-term goals, beating inflation is essential, and ignoring it can lead to a major gap between expected and actual returns.

Not Reviewing or Adjusting Investment Horizon

Financial goals and life situations change over time, but many investors set their horizon once and never review it. Not adjusting your investments when timelines shift can lead to unnecessary risks or missed opportunities. Regular reviews help you stay aligned with your goals and make smarter investment decisions.

Match Your Goals with the Right Timelines

Matching your financial goals with the right timelines is the simplest way to invest wisely and build wealth with confidence. When your money is aligned with your goals, every investment works with purpose, balancing growth, safety, and time. It’s not about chasing returns; it’s about planning smartly. If you’re unsure where to begin, talk to a Profito financial advisor to create a time-aligned strategy that fits your goals perfectly.

FAQs

What is an investment time horizon?

An investment time horizon is the period you plan to keep your money invested before using it. It helps decide the right investment type and risk level.

Why is investment horizon important in financial planning?

It determines how much risk you can take and what returns you can expect. Choosing the wrong time horizon can impact your goals and overall wealth.

How do I select the right investment horizon?

Identify your financial goal and when you need the money. Short-term needs require safer investments, while long-term goals can benefit from growth assets.

Can my investment horizon change over time?

Yes. Life events such as marriage, retirement, or children’s education may change your goals. Reviewing your horizon regularly ensures your investments stay relevant.

What is a short-term investment horizon?

It is a period of less than three years, where safety and liquidity are the main priorities.

What is a long-term investment horizon?

A long-term horizon is typically seven years or more, which allows for market growth, compounding, and higher wealth creation.

How does risk tolerance impact investment horizons?

Investors who are comfortable with market fluctuations may choose a longer horizon with equities, while conservative investors may opt for shorter horizons with stable assets.

Which is better: SIP or lump sum for long-term horizons?

SIPs are better for long-term horizons as they reduce market timing risk and benefit from compounding.

How does Profito help in deciding investment horizons?

Profito analyses your goals, risk capacity, and financial timeline to recommend the ideal horizon and asset allocation strategy.

Can I have multiple investment horizons?

Yes, each goal like buying a house, education, or retirement, can have its own horizon and investment strategy.

How often should I review my investment plan?

A review once a year or after major life changes is recommended to keep investments aligned with goals.

Why choose Profito for investment planning?

Profito offers goal-based financial advisory, helping you structure investments according to time horizons, risk appetite, and wealth-creation objectives.